Despite the ‘new normal’ of higher interest rates, 2023 will continue to offer valuable opportunities to real estate investors who are strategic in their property selection.

he relentless string of rate hikes kicked off by the Reserve Bank of Australia (RBA) in May last year has had a significant impact on a number of residential property markets across Australia.

However, despite economic headwinds, there are several key factors that continue to shape opportunities across some of our capital cities.

Here are the three drivers I believe will influence residential property investment opportunities in the year ahead.

Driver 1: Affordability

Interest rates have no doubt dampened activity across several of our residential markets. However, this impact has been far from uniform.

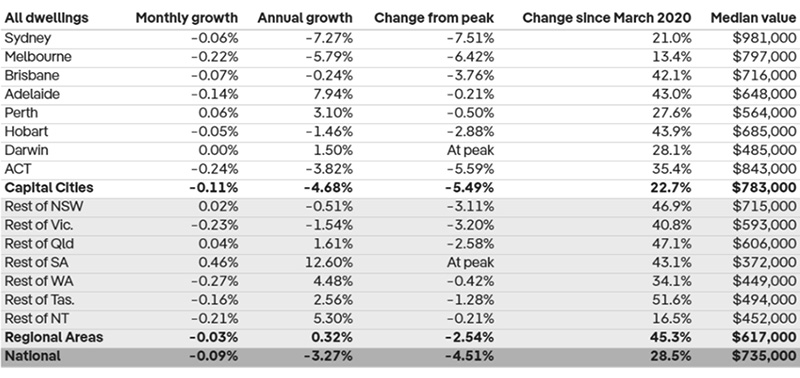

The more affordable state capitals, in particular Perth, Adelaide and Darwin, outperformed the more expensive cities in 2022, and according to PropTrack (REA Group) data, Perth was the only state capital to have continued recording price gains in January 2023.

Residential property performance to 31 January 2023

Affordability will be a critical factor this year as homebuyers and investors face the combined impact of higher rates and high inflation.

Higher interest rates don’t just affect a borrower’s repayments, they can also reduce borrowing capacity. The upshot is that many investors may look to more affordable markets, where their money stretches further and it’s possible to buy with a smaller loan.

The Real Estate Institute of Australia (REIA) monitors housing and rental affordability in all states and territories and publishes the results quarterly.

Here too, the more affordable states (notably the Northern Territory and Western Australia) stand out, with home loan repayments taking up around 31 per cent of income compared to as much as 51.6 per cent in New South Wales in the three months to September 2022. The Australian Capital Territory, despite its high median house price, is also relatively affordable due to the high average income of its residents.

Driver 2: Population growth

Population growth (particularly from migration) is a powerful driver of rental demand and rental price growth in the short to medium term. Most migrants rent when they first arrive in a new city.

The Federal Government has planned for 195,000 visa places this year, however China’s announcement that it will no longer recognise degrees obtained from foreign institutions online, meaning that students need to return to face-to-face learning, could considerably boost these numbers.

Most major centres around Australia are already experiencing extremely low vacancy rates. Data from CoreLogic and SQM research confirms that Perth has the nation’s lowest vacancy rate (0.5 per cent), while Adelaide and Hobart also have vacancy rates below 1 per cent. Population growth will continue to place pressure on the rental market and we will see increases in rental prices in most jurisdictions in 2023.

Rental market data – capital cities

| City | Sydney | Melbourne | Brisbane | Perth | Adelaide | Canberra | Darwin | Hobart |

|---|---|---|---|---|---|---|---|---|

| Vacancy rate* | 1.8% | 1.7% | 1.1% | 0.5% | 0.6% | 1.9% | 1.5% | 0.6% |

| 12-month increase in rents^ | 11.4% | 9.6% | 13.4% | 12.9% | 11.2% | 4.3% | 5.1% | 5.3% |

| Gross rental yield** | 3.2% | 3.3% | 4.3% | 4.8% | 4.0% | 4.1% | 6.3% | 4.2% |

Driver 3: The economy and job market

A healthy economy is good for residential property markets. Job opportunities are a key driver of population growth, while stronger wages and wage growth support greater resilience to interest rate rises.

On this front, several of our markets remain well-placed for 2023.

While interest rates dampen domestic economic activity, we have seen sustained growth in our exports, such that Australia now records substantial trade surpluses. Those states with a large trade exposure are also those most likely to be resilient to the slowdown in domestic demand.

WA, Queensland and the Northern Territory are our most trade-exposed markets, and most likely to benefit from the continued growth in exports.

National property market’s bottom line

In the early months of 2023, I believe we will continue to see our more expensive cities grapple with the impact of rising interest rates.

However, with inflation anticipated to be nearing its peak, I expect the major residential markets to bottom out within the first six to nine months of the year.

In the meantime, many investors will be turning their attention towards our more affordable markets, where the benefits of lower entry costs and tightening rental vacancies are driving attractive opportunities from both a yield and growth perspective.

source: apimagazine